May 31, 2024

The flash PMI data for May from S&P Global brought encouraging news on economic growth, with output of the combined manufacturing and service sectors rising across the four major developed economies – the ‘G4’ – at the fastest rate for a year. Inflation pressures meanwhile eased, down to one of the lowest levels for over three years. The rate of inflation signaled nevertheless remained stubbornly by pre-pandemic standards, having been stuck in a narrow but elevated range over the past year. There were, however, some notable variations in the growth, and most importantly, the inflation trends among the four economies.

G4 growth hits 12-month high

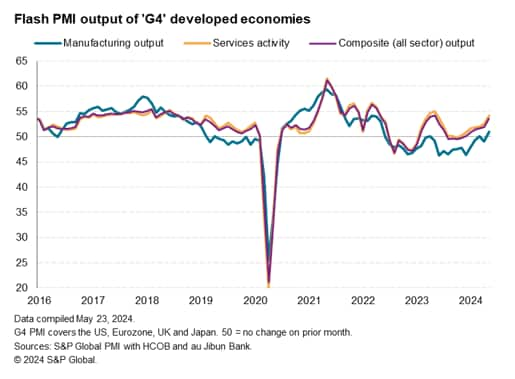

Economic growth accelerated across all four largest developed economies in May, as indicated by the GDP-weighted average PMI Output Index climbing from 50.5 in April to 52.0, its highest for a year and indicative of rising output for a fifth successive month.

The index is calculated by S&P Global from its proprietary business surveys conducted in the US, the Eurozone in association with HCOB, Japan (in association with au Jibun Bank) and the UK. Data were collected 13-21 May.

The improvement was led by the service sector, where output rose for a seventh straight month in May, growing at the sharpest rate for a year. However, manufacturing showed signs of reviving, as factory production recording the first noteworthy increase for two years.

US leads the upturn

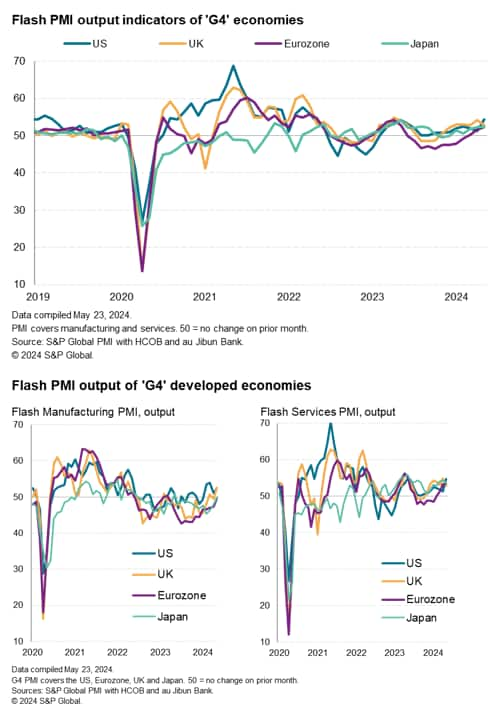

Among the four economies, the strongest expansion in May was recorded in the US, where output rose at the sharpest rate for just over two years. A 12-month high rate of expansion in the service sector was accompanied by a swelling upturn in US manufacturing, which reported the largest output rise for 13 months.

Similar, more modest, rates of growth were meanwhile seen in the UK, Eurozone and Japan, but whereas UK growth slowed, the latter two economies reported increased rates of expansion.

The eurozone’s expansion hit a 12-month high as a services led upturn was joined by a near-stabilization of factory output (where the decline was the smallest for 14 months). The improvement means output has now risen for three successive months across the region to add to signs that the malaise seen late last year has ended.

Japan’s expansion was meanwhile the strongest for nine months, the rate of growth ticking higher compared to April as sustained, but slower, services growth was met with a near steadying of manufacturing production, which reported the smallest decline for a year.

While UK growth slowed, April’s expansion had been the sharpest for a year, meaning the overall rate of growth in May remained among the highest seen over the past two years. That said, the country’s services expansion slowed markedly, a loss of pace that was in part offset by an export-bolstered jump in manufacturing output, which registered the sharpest upturn for just over two years.

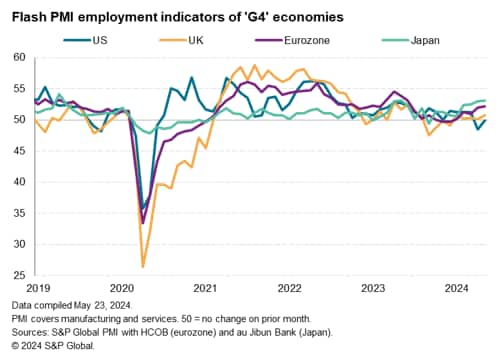

Employment rises in Europe and Japan, but dips lower in the US

Looking ahead, G4 future output expectations ticked higher in May after having slipped to a four-month low in April, lifting in all four economies bar Japan. Inflows of new business also accelerated, rising at the steepest rate for 11 months as further order book gains were seen across all four economies.

The improved order book situation and revived outlook prompted companies across the G4 to raise employment at an increased rate on average, though the overall payroll gain was still subdued by standards seen this time last year, in part reflecting tight labor markets and elevated levels of uncertainty, often linked to concerns over geopolitics and monetary policy.

However, regional variations were again noteworthy. Most notably, employment fell in the US for a second month. Although only marginal, the recent decline in employment in the US is the first seen since the early days of the pandemic. By contrast, robust and accelerating job gains were seen in the eurozone and Japan, with rates of job creation hitting 11- and 12-month highs respectively. UK jobs growth meanwhile remained muted, albeit the second-highest over the past ten months.

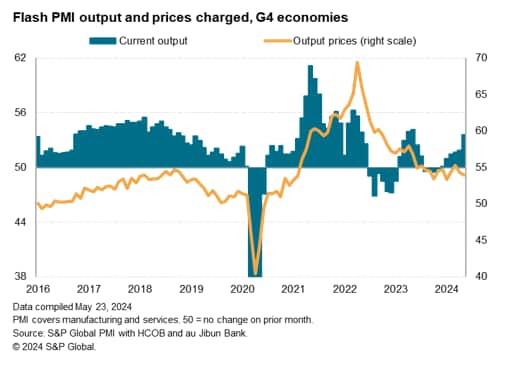

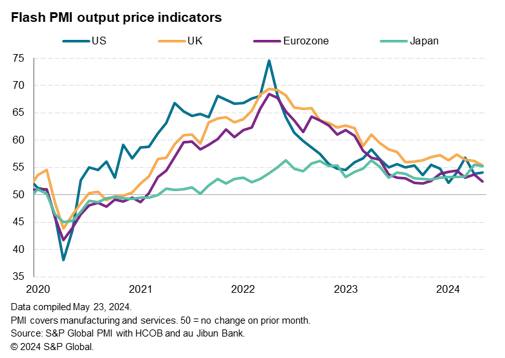

Stubborn inflation picture

From an inflation perspective, May also brought mixed news across the G4. Looking at average prices charged for goods and services, across the four economies the selling price index edged down to a four-month low yet remained very close to the average recorded over the past ten months. Much of the past year has seen price rises fluctuate in a narrow band which has been substantially above the pre-pandemic average.

The eurozone reported the slowest rate of increase of the G4 in May, with prices rising at the weakest pace since November 2023 and one of the slowest rates seen since the pandemic. Particularly encouraging was a slowing of eurozone service sector inflation to the joint-lowest in three years.

The rate of selling price inflation also remained relatively muted in the US, albeit with the rate of inflation ticking higher slightly. The rate of increase in the US nevertheless remains the lowest of the G4 economies relative to their pre-pandemic averages, notably in the case of the service sector.

Rates of inflation meanwhile cooled slightly in the UK and Japan, with the former in particular reporting a waning in the rate of increase to a 39-month low, assisted by an all-important moderation of services inflation (from a central bank policy perspective) to the lowest for just over three years. Both the UK and Japan are nevertheless continuing to see selling price inflation remain especially elevated relative to pre-pandemic averages, the latter close to all-time PMI survey highs, hinting at some stubbornness of inflation that could have a hawkish bearing on policy to a greater degree than in the case of the US and eurozone.

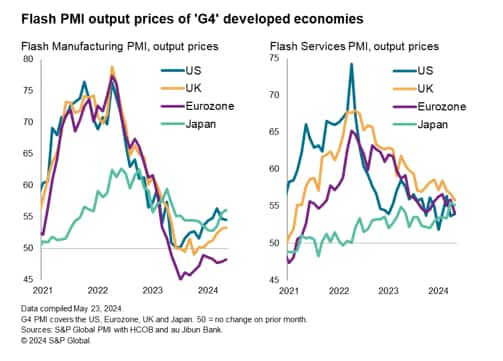

Also of note in the flash PMI results was a divergence of manufacturing selling price trends. A further disinflationary picture in the eurozone contrasted with accelerating price momentum in the UK and Japan and a further robust price gain in the US. Both the US and Japan are also notable in now seeing manufacturing price inflation exceed that of services, pointing to a potential renewed concern over the impact of rising commodity, materials and goods prices on inflation.

Data hint at cautious policymaking

In summary, the major developed economies are showing signs of gaining further growth momentum on average midway through the second quarter, but employment growth is somewhat subdued as companies either await further clarity on the outlook or struggle to find suitable staff, the latter issues appearing most prominent in the US and UK. Nonetheless, the rise in employment bodes well for the upturn to be sustained and is supported by brighter news on order books and business confidence in May.

Inflation meanwhile remains elevated by pre-pandemic standards across all G4 economies, albeit to greater extents in the UK and Japan than the US and the eurozone. While service sector inflation rates are generally trending lower, which will be welcome news to policymakers concerned over second-round wage-related price pressures, there are signs of renewed price pressures appearing in manufacturing, albeit not yet in the eurozone.

As such, the reviving growth trend and worryingly slow descent of inflation hints at some continued caution among policymakers in the US and Europe in loosening monetary policy, especially as some policymakers may be keen to see how stronger growth impacts pricing power and wage negotiations.

Source: S&P – by Chris Williamson

Legal Notice: The information in this article is intended for information purposes only. It is not intended for professional information purposes specific to a person or an institution. Every institution has different requirements because of its own circumstances even though they bear a resemblance to each other. Consequently, it is your interest to consult on an expert before taking a decision based on information stated in this article and putting into practice. Neither Karen Audit nor related person or institutions are not responsible for any damages or losses that might occur in consequence of the use of the information in this article by private or formal, real or legal person and institutions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}