Source: Corporate Tax Law Communiqué No. 23

Legal Notice: The information in this article is intended for information purposes only. It is not intended for professional information purposes specific to a person or an institution. Every institution has different requirements because of its own circumstances even though they bear a resemblance to each other. Consequently, it is your interest to consult on an expert before taking a decision based on information stated in this article and putting into practice. Neither Karen Audit nor related person or institutions are not responsible for any damages or losses that might occur in consequence of the use of the information in this article by private or formal, real or legal person and institutions.

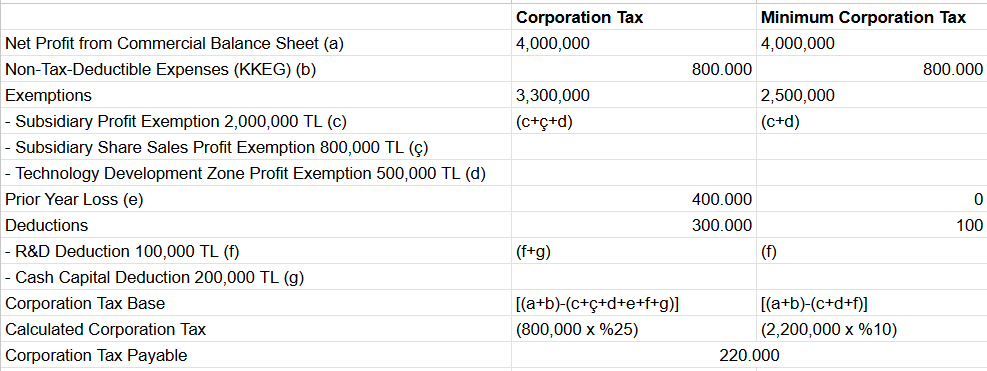

Domestic Minimum Corporate Tax in Türkiye – Example 3 (In Case of Profit, Non-tax-Deductible Expenses, Dividend Exemption, 4691 Technopark Exemption, R&D Deduction, Cash Capital Deduction, and Prior Year Loss)

Domestic Minimum Corporate Tax Example-3

Related Posts

March 2025 Business Confidence in Finland: Sectoral Insights – Manufacturing Improves, Construction Declines, Services and Retail Show Modest Gains

Gallery

{kind=link}

{kind=link}

{kind=link}

{kind=link}