October 13, 2023,

Higher-for-Longer Interest Rate Environment is Squeezing More Borrowers

The world’s central banks have unleashed the steepest series of interest-rate increases in decades during their two-year drive to tame inflation—and they may not be done yet. Policymakers have raised rates by about 400 basis points on average in advanced economies since late 2021, and around 650 basis points in emerging market economies.

Most economies are absorbing this aggressive policy tightening, showing resilience over the past year, but core inflation remains elevated in several of them, especially the United States and parts of Europe. Major central banks therefore may need to keep interest rates higher for longer.

In this environment, risks to the world economy remain skewed to the downside, as we detail in in our Global Financial Stability Report. Though this latest assessment of vulnerabilities is similar to what we noted in April, the acute stress we saw in some banking systems has since subsided. However, we now see indications of trouble elsewhere.

One such warning sign is the diminished ability of individual and business borrowers to service their debt, also known as credit risk. Making debt more expensive is an intended consequence of tightening monetary policy to contain inflation. The risk, however, is that borrowers might already be in precarious positions financially, and the higher interest rates could amplify these fragilities, leading to a surge of defaults.

Eroding buffers

In the corporate world, many businesses suffered closures during the pandemic, and others emerged with healthy cash buffers thanks in part to fiscal support in many countries. Firms were also able to protect their profit margins even though inflation had picked up. In a higher-for-longer world, however, many firms are drawing down cash buffers as earnings moderate and as debt servicing costs rise.

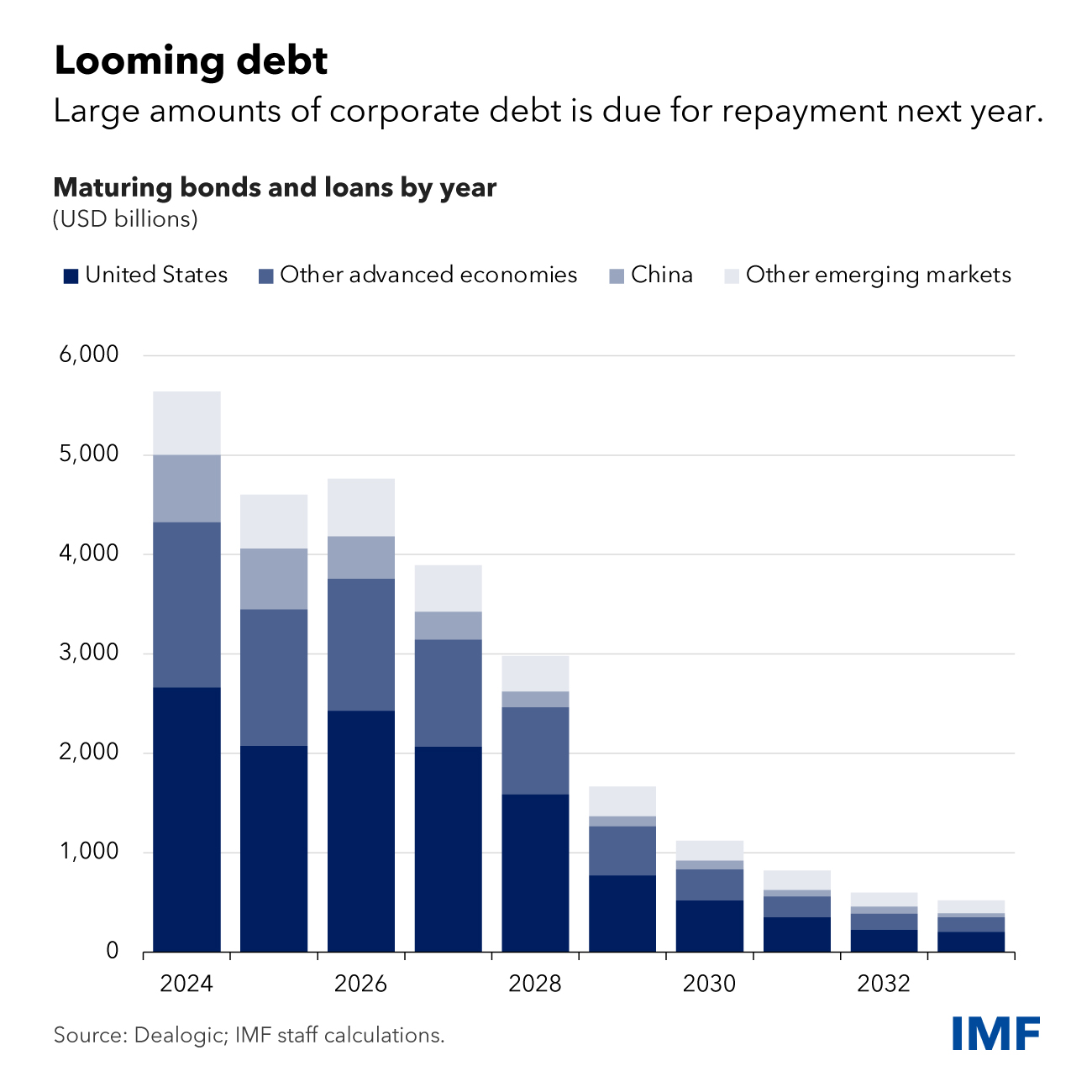

Indeed, the GFSR shows increasing shares of small and mid-sized firms in both advanced and emerging market economies with barely enough cash to pay their interest expenses. And defaults are on the rise in the leveraged loan market, where financially weaker firms borrow. These troubles are likely going to worsen in the coming year as more than $5.5 trillion of corporate debt comes due.

Households too have been drawing down their buffers. Excess savings in advanced economies have steadily declined from peak levels early last year that were equal to 4 percent to 8 percent of gross domestic product. There are also signs of rising delinquencies in credit cards and auto loans.

Headwinds also confront real estate. Home mortgages, typically the largest category of household borrowing, now carry much higher interest rates than just a year ago, eroding savings and weighing on housing markets. Countries with predominantly floating rate mortgages have generally experienced larger home price declines as higher interest rates translate more quickly into mortgage payment difficulties. Commercial real estate faces similar strains as higher interest rates have resulted in funding sources drying up, transactions slowing, and defaults rising.

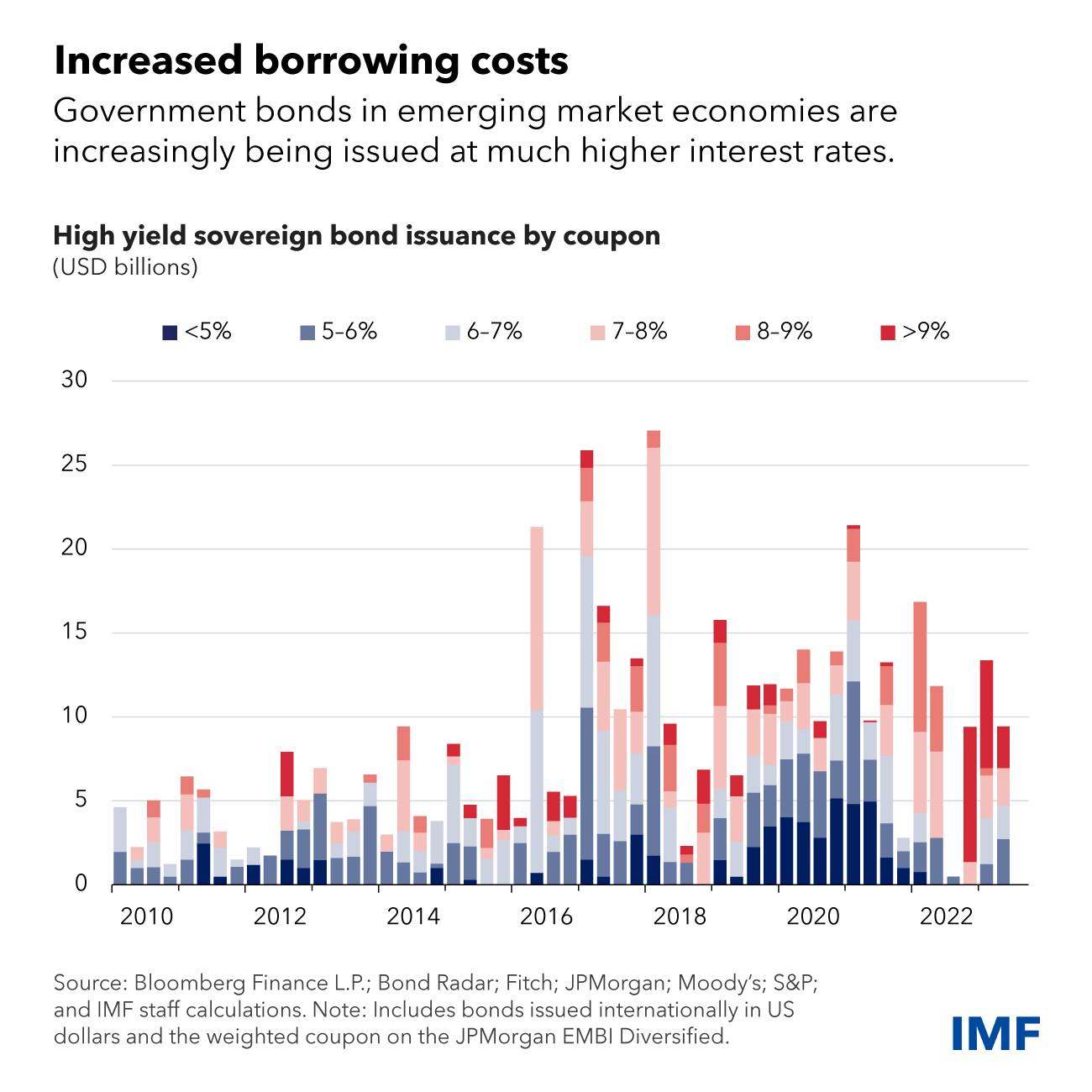

Higher interest rates also are challenging governments. Frontier and low-income countries are having a harder time borrowing in hard currencies like the euro, yen, US dollar and UK pound as foreign investors demand greater returns. This year, hard currency bond issuances have occurred at much higher coupon—or interest—rates. But sovereign debt concerns do not only apply to low-income countries, as the recent surge in longer-term interest rates in advanced economies has demonstrated.

By contrast, major emerging economies largely do not face this predicament given better economic fundamentals and financial health, although the flow of foreign portfolio investment into these countries has also slowed. Material amounts of foreign investment have left China in recent months as mounting troubles in its property sector have dented investor confidence.

Spillover effects

Most investors appear to have shrugged off mounting evidence that borrowers are having repayment troubles. Along with generally healthy stock and bond markets, financial conditions have eased as investors appear to expect a global soft landing, in which higher central bank interest rates contain inflation without causing a recession.

This optimism creates two problems: relatively easy financial conditions could continue to fuel inflation, and rates can tighten sharply if adverse shocks occur—such as an escalation of the war in Ukraine or an intensification of stress in the Chinese property market.

A sharp tightening of financial conditions would strain weaker banks already facing higher credit risks. Surveys from several countries already point to a slowdown in bank lending, with rising borrower risk cited as a key reason. Many banks will lose significant amounts of equity capital in a scenario where high inflation and high interest rates prevail and the global economy tips into recession, as we explore in a forthcoming GFSR chapter. Investors and depositors will scrutinize the prospects of banks if their stock-market capitalization falls below the value of balance sheet, causing funding problems for the weak bank. Outside of banking system, fragilities are also present for nonbank financial intermediaries, such as hedge funds and pension funds, that lend in private markets.

Reassuringly, policymakers can prevent bad outcomes. Central banks must remain determined in bringing inflation back to target—sustained economic growth and financial stability is not possible without price stability. If financial stability is threatened, policymakers should promptly use liquidity support facilities and other tools to mitigate acute stress and restore market confidence. Finally, given the importance of healthy banks to the global economy, there is a need to further enhance financial sector regulation and supervision.

Source: IMF BLOG – by Tobias Adrian

Legal Notice: The information in this article is intended for information purposes only. It is not intended for professional information purposes specific to a person or an institution. Every institution has different requirements because of its own circumstances even though they bear a resemblance to each other. Consequently, it is your interest to consult on an expert before taking a decision based on information stated in this article and putting into practice. Neither Karen Audit nor related person or institutions are not responsible for any damages or losses that might occur in consequence of the use of the information in this article by private or formal, real or legal person and institutions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}