October 6, 2023

Inflation around the world reached multi-decade highs last year. While headline inflation is coming down steadily, core measures―which exclude food and energy―are proving stickier in many economies and wage growth has picked up.

Expectations about future inflation play a key role in driving inflation, as those views influence decisions about consumption and investment which can affect price and wages today. How best to inform people’s views on inflation became an even more crucial consideration as the surge in prices fueled concern that inflation could become entrenched.

In an analytical chapter of the latest World Economic Outlook, we examine how expectations affect inflation and the scope for monetary policy to influence these expectations to achieve a ‘soft landing,’ that is, a scenario where a central bank guides inflation back to its target without causing a deep downturn in growth and employment.

Larger role for inflation expectations

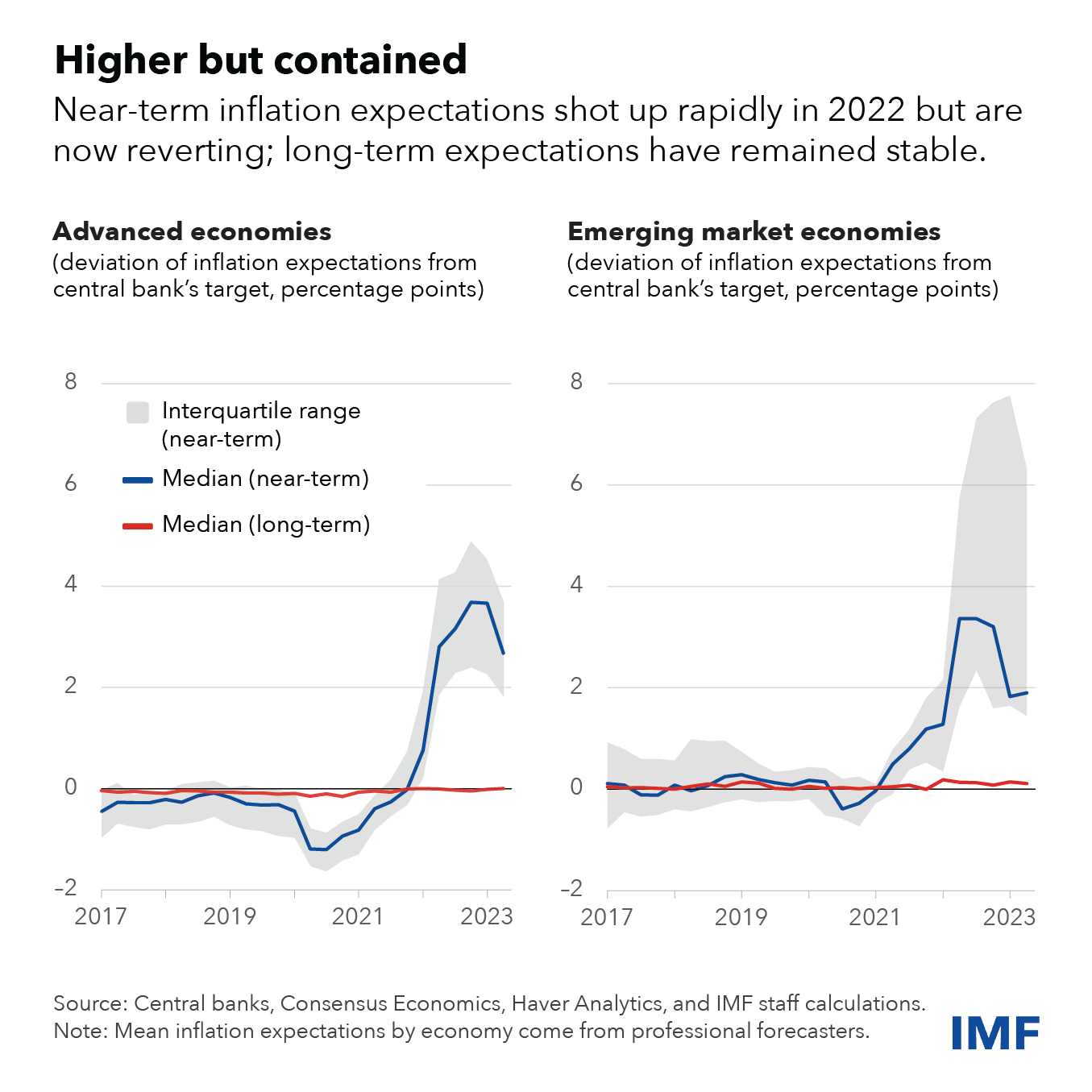

Surveys of professional forecasters have shown that expectations for inflation over the next 12 months—near-term expectations—started a steady rise in 2021 in advanced and emerging market economies alike, then accelerated last year as actual price increases gained momentum. Expectations for inflation five years into the future, however, remained stable, with average levels broadly anchored around central bank targets.

More recently, near-term inflation expectations appear to have turned the corner and begun to shift onto a gradual downward path. Beyond the world of professional forecasters, we see similar patterns of inflation expectations by companies, individuals, and financial-market investors, on average.

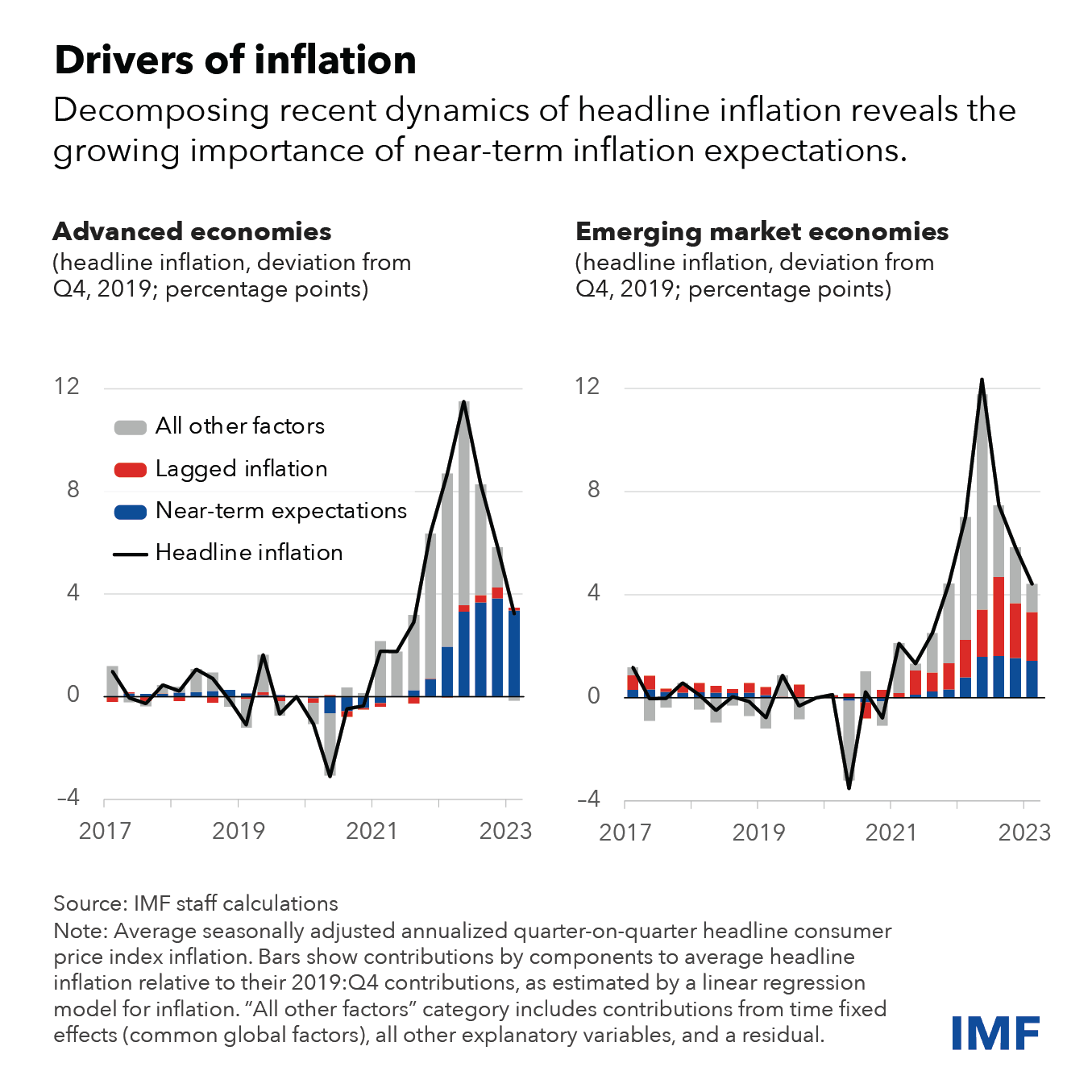

Movements in near-term expectations are economically important for inflation dynamics. According to our new statistical analysis, after the inflationary shocks in 2021 and early 2022 started unwinding late last year, inflation has been increasingly explained by near-term expectations.

For the average advanced economy, they now represent the primary driver of inflation dynamics. For the average emerging market economy, expectations have grown in importance, but past inflation remains more relevant, suggesting that people may be more backward-looking in these economies. This could reflect in part the historically higher and more volatile inflationary experience in many of these economies.

In fact, we find that inflation in advanced economies typically rises by about 0.8 percentage points for each 1 percentage point rise in near-term expectations while the pass-though is only 0.4 percentage points in emerging market economies.

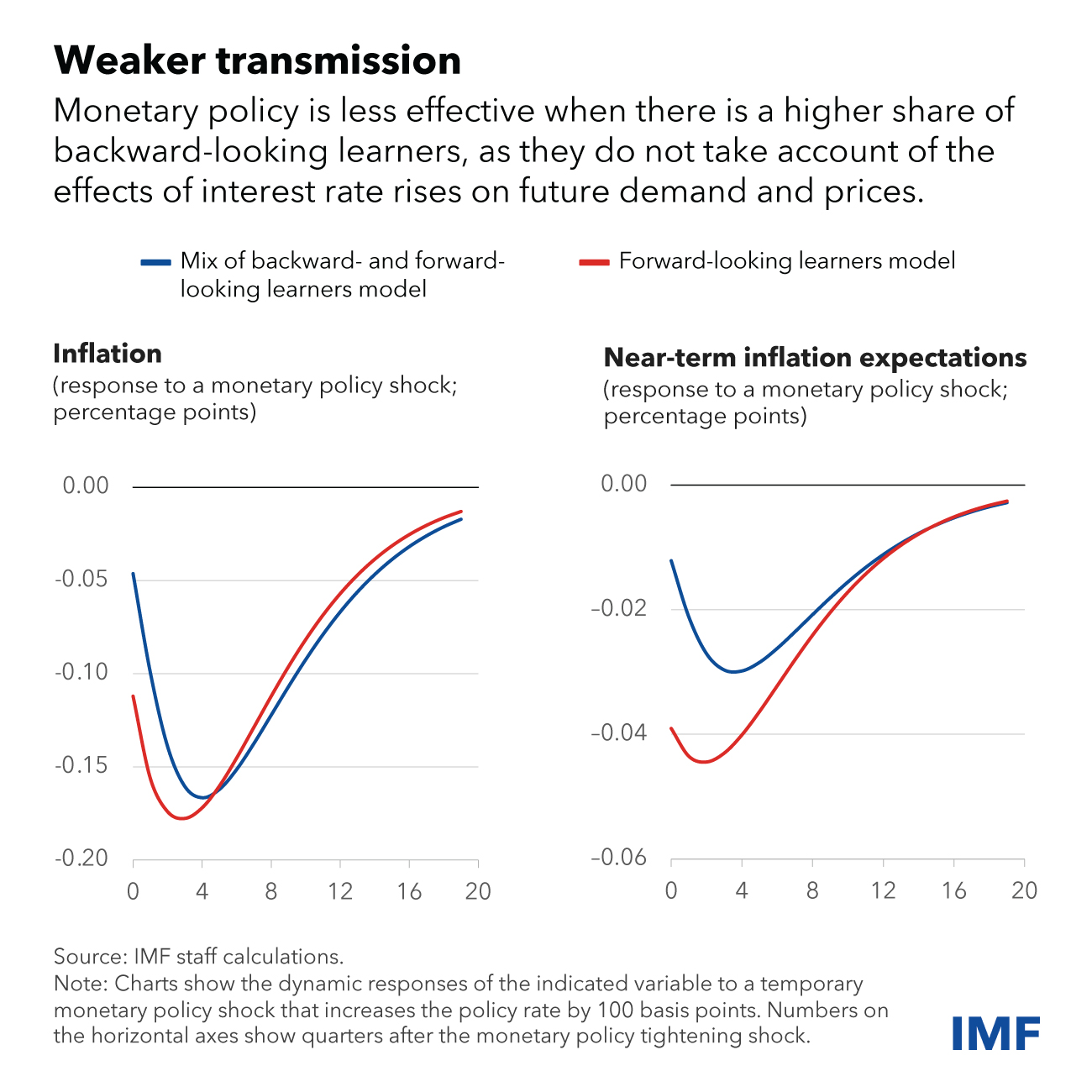

One factor that could account for this difference is the share of backward-looking versus forward-looking learners across economy groups. When information on inflation prospects is scarce and central bank communications are unclear or lack credibility, people tend to form their views about future price changes based on their current or past inflation experiences—they are more backward-looking learners. By contrast, those who are more forward-looking form their expectations from a broader array of information that could be relevant to future economic conditions, including central bank actions and communications—they are more forward-looking learners.

Policy implications of differences in learning

These differences have important consequences for central banks. As shown in simulations from a new model that allows for differences in learning and expectations formation, policy tightening has less of a dampening effect on near-term inflation expectations and inflation when a greater share of people in the economy are backward-looking learners.

That’s because people more focused on the past do not internalize the fact that interest rate increases today will slow inflation as they weigh on demand in the economy. Therefore, a higher share of backward-looking learners means that the central bank must tighten more to get the same decrease in inflation. In other words, reductions in inflation expectations and inflation come at a higher cost to output when there is a higher share of backward-looking learners.

Enhancing policy effectiveness

Central banks can encourage expectations to be more forward-looking through improvements in the independence, transparency, and credibility of monetary policy and by communicating more clearly and effectively. Such changes help people understand the central bank’s policy actions and their economic effects, boosting the share of forward-looking learners in the economy.

Simulations from the new model show how improvements in monetary policy frameworks and communications can help lower the output costs needed to reduce inflation and inflation expectations, making it more likely the central bank can achieve a soft landing.

One way central banks can improve their communications is by simple and repeated messaging about their objectives and actions that is tailored to the relevant audiences.

However, improving monetary policy frameworks and crafting new tailored communication strategies to help improve inflation dynamics can take time or be difficult to implement. Such interventions are complementary to more traditional monetary policy tightening actions, which will remain key to bringing inflation back to target in a timely manner.

Source: IMF BLOG – by Silvia Albrizio, John Bluedorn

Legal Notice: The information in this article is intended for information purposes only. It is not intended for professional information purposes specific to a person or an institution. Every institution has different requirements because of its own circumstances even though they bear a resemblance to each other. Consequently, it is your interest to consult on an expert before taking a decision based on information stated in this article and putting into practice. Neither Karen Audit nor related person or institutions are not responsible for any damages or losses that might occur in consequence of the use of the information in this article by private or formal, real or legal person and institutions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}